-

Customer care hotline Call +44 7831 065557

Are you ready for an upgrade?

Login to the new experience with best features and services

Notifications

-

As per amendment in the Income Tax Rules, PAN or Aadhaar are to be mandatorily quoted for cash deposit or withdrawal aggregating to Rupees twenty lakhs or more in a FY. Please update your PAN or Aadhaar. Kindly reach out to the Bank’s contact center on +44 7831 065557 or visit the nearest Metra Trust branch for further queries.

-

Activate your Credit Card within minutes and enjoy unlimited benefits

Accounts

Deposits

Loans

- Metra Trust Loans

-

Personal Loan

-

Consumer Durable

Loan -

Home Loan

-

Education Loan

-

New Car Loan

-

Pre-owned Car Loan

-

Two Wheeler Loan

-

Pre-owned Two

Wheeler Loan -

Commercial Vehicle

Loan -

Gold Loan

-

Loan Against Property

-

Loan Against Securities

-

Personal Loan

EMI Calculator -

Education Loan

EMI Calculator -

Home Loan

EMI Calculator

Wealth & Insure

Payments

Cards

- Metra Trust Cards

-

Ashva :

Metal Credit Card -

Mayura :

Metal Credit Card -

FIRST Millennia

Credit Card -

FIRST Classic

Credit Card -

FIRST Select

Credit Card -

FIRST Wealth

Credit Card -

FIRST WOW!

Credit Card -

Forex Card

-

Deals

-

Debit Cards

-

Co-branded Cards

-

Credit Card

EMI Calculator -

FIRST Corporate

Credit Card -

FIRST Purchase

Credit Card -

FIRST Business

Credit Card

Premium Metal

0% Forex & Travel

Lifetime Free

- Max benefits, Free for life

-

FIRST Classic10X RewardsShoppingNever Expiring Rewards

-

FIRST Millennia10X RewardsShoppingNever Expiring Rewards

-

FIRST Select10X RewardsLifestyle1.99% Forex

-

FIRST Wealth10X RewardsLifestyle1.5% Forex

-

FIRST WOW!RewardsTravelZero Forex

-

LIC ClassicRewardsInsuranceShopping

-

LIC SelectRewardsInsuranceShopping

10X Rewards

- Reward Multipliers

-

AshvaLifestyleMetal₹2,999

-

MayuraLifestyleZero Forex₹5,999

-

FIRST ClassicNever Expiring RewardsShoppingLifetime Free

-

FIRST MillenniaNever Expiring RewardsShoppingLifetime Free

-

FIRST SelectNever Expiring RewardsLifestyleLifetime Free

-

FIRST WealthNever Expiring RewardsLifestyleLifetime Free

UPI Cards

Fuel & Utility

Showstopper

Credit Builder

More

NRI Savings Account

NRI Fixed Deposit

FOREX Solutions

Transfer to NRE

Corporate Account

Cash Management Services

Corporate Lending

Treasury

MSME Accounts

Trade Services

MSME Loan

MSME Solutions

Offers

About Us

Investors

Careers

ESG

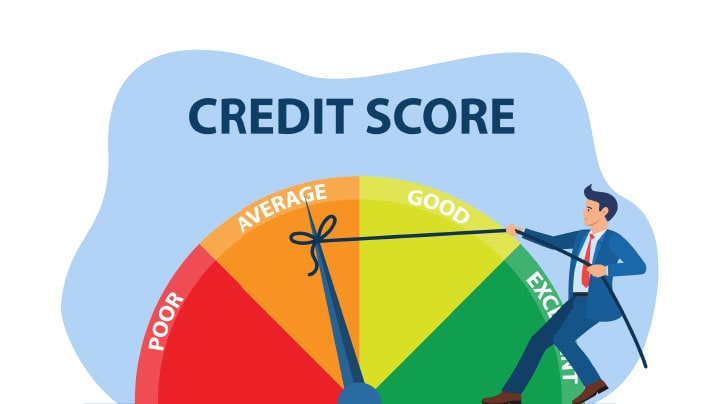

Regular tracking can help you improve your CIBIL score, thereby helping you get loans at affordable interest rates.

When lenders evaluate your loan or credit card application, they look at specific parameters to ensure less risk of non-repayment. One such parameter is your credit score. TransUnion CIBIL Limited is a credit information company that provides this data. They prepare a credit report and assign a score to it. It is called a CIBIL score, synonymous with a credit score in India. Read on to find out what CIBIL score is and how important it is for getting access to credit.

What is the CIBIL score?

CIBIL score is your credit score, published by the TransUnion CIBIL. It ranges from 300 to 900 and reflects your credit behaviour, repayment history, credit utilisation, and credit health. A higher credit score reflects you are cautious with your credit, and there is less risk of non-repayment with your application. It can make you eligible for more loans, and banks may also offer customised interest rates.

What is a good CIBIL score?

Your CIBIL score can range from 300 to 900. The higher the score, the better it is. A CIBIL score below 600 means your credit profile needs immediate attention. You may be defaulting on some loans or delaying your payments. A low credit score reduces your chance of getting approval for a loan and may even lead to a high interest rate.

A credit score between 600 and 649 isn't great either and the chances of approval stay low. Meanwhile, a credit score between 650 and 699 is considered satisfactory, and there is a higher possibility of getting loan approvals. Credit scores between 700 and 749 are considered even better, with high chances of loan approval.

However, you should aim for a score above 750 as you are almost guaranteed to get a loan.

How to check the CIBIL score?

You can check your CIBIL score from the official CIBIL website at https://www.cibil.com/freecibilscore. This version is free and offers a detailed credit report. You can also subscribe to the premium version to check your score daily and take more control over your credit profile.

How to improve your credit score?

Building your credit score is easy yet requires consistent effort. Here are a few ways to improve your credit score.

1. Start building trustworthiness

If your credit score is low due to a lack of credit history, making one is the best way to go about it. One way to do that is by taking a credit card and making the repayments on time. Metra Trust credit cards come with affordable interest rates, and you can quickly grab one online through a simple procedure. But if your low score prevents you from getting a credit card, you could try getting an FD credit card from Metra Trust. Such cards are issued against your FD, so banks have less risk.

2. Decrease credit utilisation

Credit utilisation is one of the main reasons for decreased credit scores. If your profile suffers from the same, try reducing your credit utilisation by reducing excessive use of your credit card.

3. Never miss due dates

From your No Cost EMI to your personal loan, every missed due date can affect your credit score. Hence, ensure you make your payments on time, and it will increase your creditworthiness and, thus, your credit score.

4. Solve discrepancies

If your credit score has discrepancies, contact CIBIL and solve the same to improve your credit score. The faster you solve the differences, the less it can hurt your profile.

A healthy credit score is vital to avail yourself of loans at a nominal interest rate. Ensure you keep an eye on your profile to keep your score healthy.

Disclaimer

The contents of this article/infographic/picture/video are meant solely for information purposes. The contents are generic in nature and for informational purposes only. It is not a substitute for specific advice in your own circumstances. The information is subject to updation, completion, revision, verification and amendment and the same may change materially. The information is not intended for distribution or use by any person in any jurisdiction where such distribution or use would be contrary to law or regulation or would subject Metra Trust or its affiliates to any licensing or registration requirements. Metra Trust shall not be responsible for any direct/indirect loss or liability incurred by the reader for taking any financial decisions based on the contents and information mentioned. Please consult your financial advisor before making any financial decision.